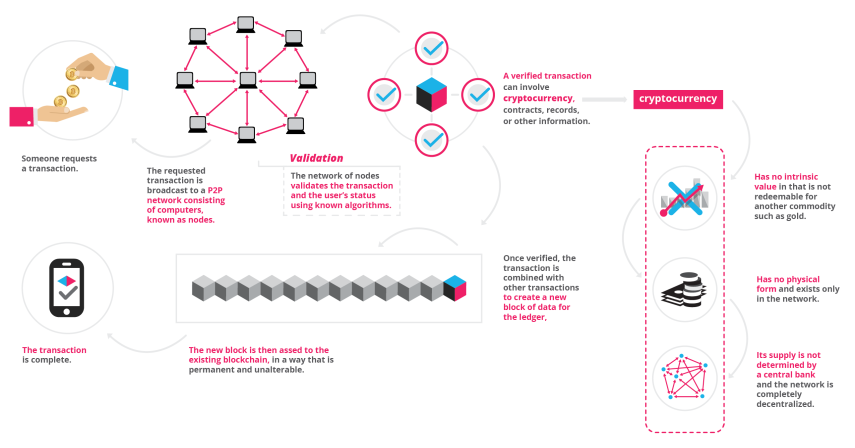

How does Blockchain technology work?

Try to picture Blockchain as a spreadsheet that is duplicated thousands of times across a network of computers, with the network designed to be updated regularly. The Blockchain exists as a shared database and is not stored in any single location, resulting in truly public and easily verifiable records. Because the system is decentralized, there is no information that a hacker can corrupt. The data is hosted by millions of computers simultaneously, and is accessible to anyone on the internet. It can be programmed to record not just financial transactions, but virtually everything of value.

How can Blockchain be useful to your business?

- Smart contracts

Chris DeRose further explains on American Banker that ‘smart contracts’ are “self-automated computer programs that can carry out the terms of any contract.” In essence, “it is a financial security held in escrow by a network that is routed to recipients based on future events, and computer code.” Businesses will be able to use ‘smart contracts’ to bypass regulations and “lower the costs for a subset of our most common financial transactions.” Best of all? These contracts will be unbreakable. Example of how smart contracts can be used is Slock.it, who help at developing the future infrastructure of the Sharing Economy

- Cloud Storage

Cloud storage will be another application that businesses can take advantage of. Storj is one such company that’s offering secure cloud storage while decreasing dependency. Storj founder Shawn Wilkinson told VentureBeat that “Simply using excess hard drive space, users could store the traditional cloud 300 times over,” much like how you can rent out your home or room on Airbnb. Wilkinson also said, “Considering the world spends $22 billion + on cloud storage alone, this could open a revenue stream for average users, while significantly reducing the cost to store data for companies and personal users.”

- Supply-Chain Communications & Proof-of-Provenance

Phil Gomes says on Edelman Digital “Most of the things we buy aren’t made by a single entity, but by a chain of suppliers who sell their components (e.g., graphite for pencils) to a company that assembles and markets the final product. The problem with this system is that if one of these components fails ‘the brand takes the brunt of the backlash.’” Using blockchain technology would “proactively provide digitally permanent, audit-able records that show stakeholders the state of the product at each value-added step.”

Provenance and SkuChain are just two examples of companies attempting resolve this issue.

- Paying Employees

Since the blockchain has it’s roots in cryptocurrency, it only makes sense that it could be used as an application to compensate employees. Geoff Weiss adds on Entrepreneur that “If your company regularly pays wages to international workers, then incorporating Bitcoin into the payroll process could be a major cost saver.”

Bitwage, which claims to be the world’s first Bitcoin-based payroll service, will “circumvent the costly fees associated with transferring money internationally, as well as the time it takes for such funds to move from bank to bank, payments made via Bitcoin can save both money and time for employers and employees alike.” Bitwage’s founder and COO, Jonathan Chester says that by using a public ledger of all transactions in chronological order “you can actually see exactly where the money is throughout the process.”

Then there is paying remote employees and contractors. This form of payments is a very large part of my personal business and something many big companies (and banks) are betting on this year.

- Electronic Voting

BitShares, a globally distributed database, states “Delegated Proof of Stake (DPOS) is the fastest, most efficient, most decentralized, and most flexible consensus model available.” BitShares goes on to state:

“DPOS leverages the power of stakeholder approval voting to resolve consensus issues in a fair and democratic way. All network parameters, from fee schedules to block intervals and transaction sizes, can be tuned via elected delegates. Deterministic selection of block producers allows transactions to be confirmed in an average of just 1 second. Perhaps most importantly, the consensus protocol is designed to protect all participants against unwanted regulatory interference.”

The future of blockchain will be growing in the coming years. Over the past six months I’ve filed over 6 patents in this space. To my surprise there had been over 1200 patents files with blockchain as a part. It’s only going to grow.

Interesting to find more about investing in cryptocurrencies such as Bitcoin? Then read our next article Understanding Bitcoin and easy steps to start investing.

—

This article was first published on execed.economist.com